The Evolution of the Streaming Wars: Consolidation, Subscription Fatigue, and the New Era of Digital Media Economics

the Equilibrium of Exhaustion

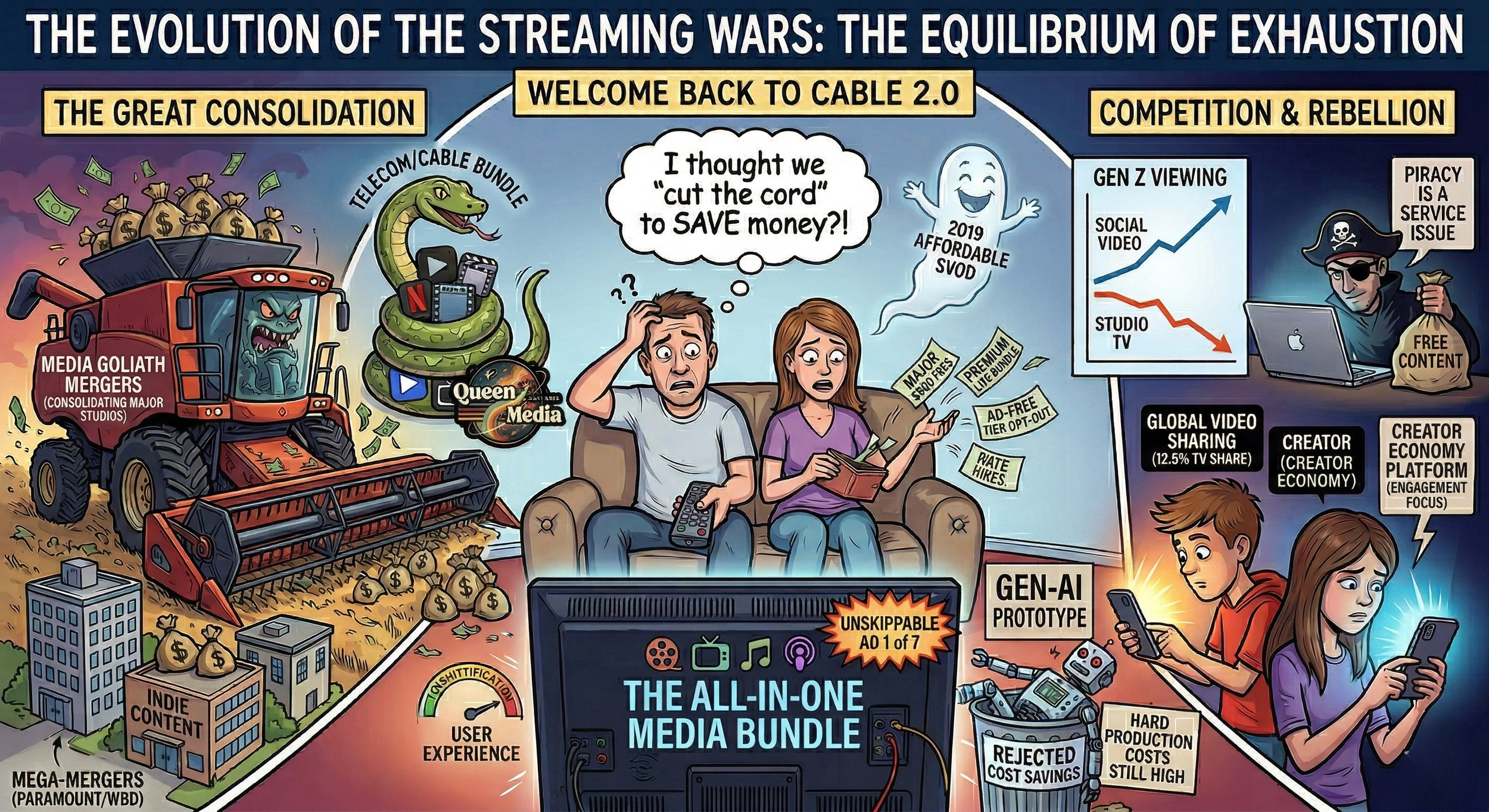

By the second quarter of 2026, the global entertainment and media streaming industry fundamentally transitioned out of its aggressive, venture-subsidized growth phase and entered a period defined by austere financial rationalization, intense market consolidation, and shifting consumer loyalties. The aggressive land grab known colloquially as the "streaming wars" is effectively over, and the industry is now navigating the complex, often highly volatile realities of the "streaming equilibrium." Strategies previously engineered to capture market share at all costs have been abruptly replaced by operating models strictly optimized for profitability, average revenue per user (ARPU) expansion, and structural churn mitigation.

This paradigm shift was catalyzed by undeniable market saturation. With major platforms having exhausted their primary pools of addressable subscription video-on-demand (SVOD) households, revenue growth has become entirely dependent on aggressive price hikes, the implementation of ad-supported video-on-demand (AVOD) tiers, and severe cost-cutting measures that have reshaped the creative output of Hollywood. Consequently, consumers are experiencing unprecedented "subscription fatigue," manifesting in soaring cancellation rates, the widespread adoption of "serial churning" behaviors, and a measurable, devastating resurgence in digital piracy.

As stand-alone SVOD economics prove increasingly fragile for all but the largest incumbent, the industry is witnessing a structural regression toward traditional aggregation. Telecommunications providers and digital aggregators are resurrecting the "cable bundle" to stabilize user retention, while free ad-supported streaming TV (FAST) channels and virtual multichannel video programming distributors (vMVPDs) capture a rapidly growing share of living-room viewing time. Simultaneously, the aggressive encroachment of social video platforms—namely YouTube and TikTok—into premium television spaces is redefining the boundaries of the entertainment sector entirely, proving that the greatest threat to legacy media is not rival studios, but the creator economy itself.

The Financial Architecture of 2026: From Acquisition to Yield

Data derived from Q4 2025 and Q1 2026 corporate disclosures prior to the cessation of regular reporting metrics by several entities.

A critical indicator of the streaming industry's maturation is the coordinated abandonment of public subscriber count reporting. Following Netflix's decision to stop publicly disclosing quarterly subscriber additions and ARPU at the end of 2024, The Walt Disney Company and Warner Bros. Discovery (WBD) followed suit in late 2025 and early 2026. This opacity marks a fundamental philosophical shift: institutional investors and Wall Street analysts are no longer rewarding raw user acquisition; the mandate is now strict financial yield, operating margins, and deeply integrated engagement metrics.

Corporate Financial Performance and the ARPU Imperative

The financial snapshot of the industry reveals a stark divide between the runaway market leader and the legacy studios fighting to construct sustainable profitability architectures.

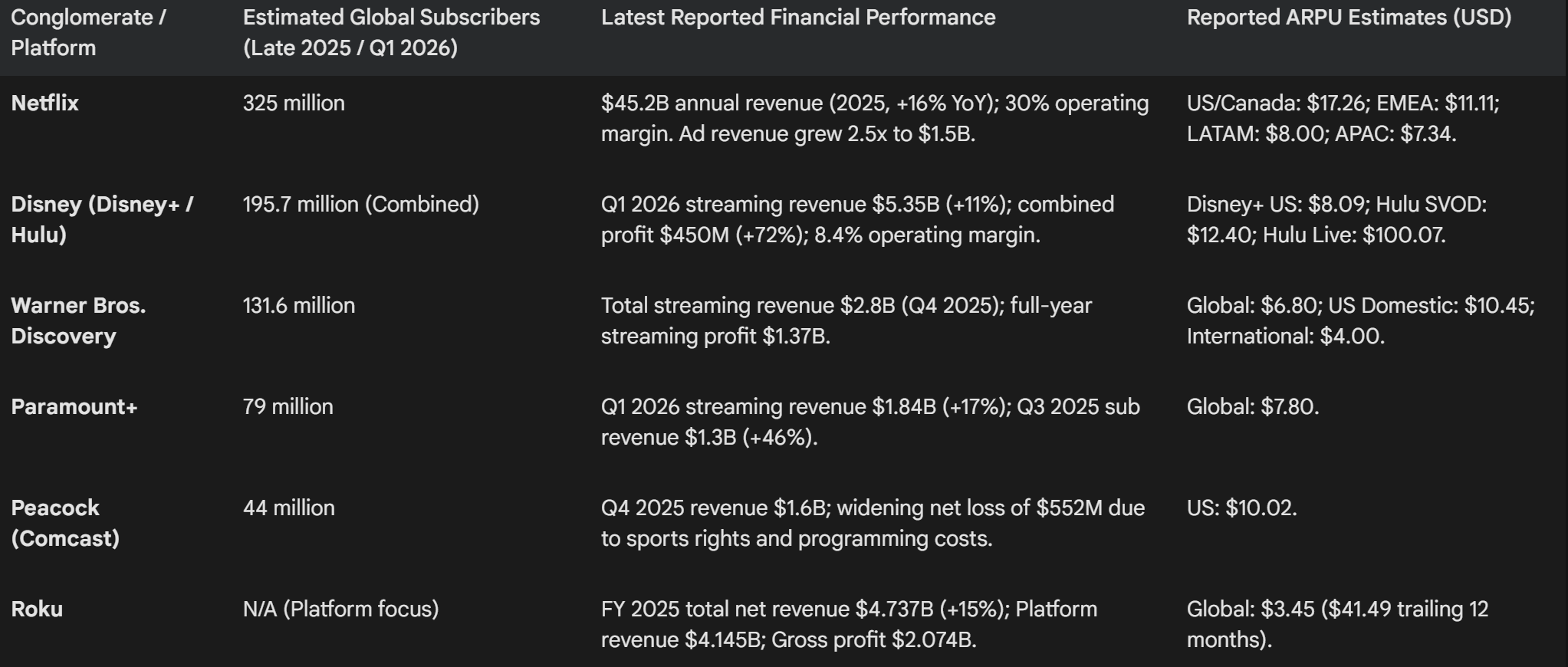

Netflix's dominance is absolute, serving as the benchmark for direct-to-consumer viability. The platform generated $45.2 billion in 2025 revenue, and management projects full-year 2026 revenue between $50.7 billion and $51.7 billion, heavily buoyed by its burgeoning advertising business and strategic price engineering. Viewers on Netflix consumed 96 billion hours of content in the second half of 2025 alone, representing an engagement moat that competitors struggle to breach.

Conversely, platforms anchored to legacy telecommunications or broadcast frameworks face severe margin pressures. Despite growing its subscriber base to a meaningful 44 million and increasing revenue to $1.6 billion, Comcast's Peacock suffered a $552 million quarterly loss in late 2025. This widening deficit was driven by the immense burden of sports rights, particularly the platform's multi-billion dollar commitments to the NBA, NFL, and Olympic broadcasting. Comcast executives remain resolute that the platform will achieve breakeven by late 2026, relying heavily on continued price increases and the integration of theatrical pay-one movie windows from Universal Pictures.

The underlying trend across all these financials is the maximization of ARPU. ARPU figures reflect a complex blend of high-paying domestic subscribers and lower-paying international users, but the consensus across all boardrooms is that ARPU must rise exponentially to justify the tens of billions spent annually in the content arms race.

Mega-Mergers and the Antitrust Gauntlet

The search for increased profitability, combined with the sheer scale required to compete in the 2026 marketplace, has forced mid-tier and even upper-tier streaming conglomerates to merge or sell. Approximately 76.5% of industry leaders surveyed by Looper Insights accurately predicted that mounting pressure to improve profitability would force mid-tier streamers to consolidate as organic growth stalled. As of early 2026, the landscape was permanently altered by two monumental transactions that underscore the prevailing economic anxieties of legacy Hollywood studios.

The $110 Billion Paramount and Warner Bros. Discovery Merger

The most tectonic shift in the media landscape culminated in Paramount Skydance's underdog acquisition of Warner Bros. Discovery (WBD) in a staggering $110.9 billion transaction. The deal, spearheaded by Paramount CEO David Ellison, snatched the WBD media empire away from a fiercely competing bid from Netflix executives Ted Sarandos and Greg Peters.

The corporate maneuvering was highly complex. Initially, WBD's board recommended a merger with Netflix, which had presented an $82.7 billion enterprise value bid ($27.75 per share) structured entirely in cash to provide "enhanced certainty". WBD initially rejected a Paramount offer from December 2025, stating that pulling out of the Netflix deal would incur a massive $4.7 billion penalty—including a $2.8 billion termination fee to Netflix, $1.5 billion for failing to complete a debt exchange, and $350 million in incremental interest.

However, following a seven-day limited waiver period granted by Netflix, Paramount returned with a drastically enhanced proposal. Paramount secured committed equity funding to offer $30.00 per share, agreed to fund the $2.8 billion break fee to Netflix, and critically, offered to fully backstop an exchange offer that relieved WBD of its $1.5 billion contractual bondholder obligations. Finding this revised offer to be the superior proposal, WBD officially pivoted, setting a shareholder vote for April 23, 2026, to finalize the Paramount transaction.

The strategic rationale behind this mega-merger is rooted entirely in achieving critical mass. The combined entity aims to bring together Paramount+ and HBO Max into a unified streaming platform poised to boast over 200 million subscribers, allowing it to compete directly with Netflix's industry-leading 325 million user base. The financial mechanics of the deal are heavily reliant on projected synergies: the combined company anticipates generating over $6 billion in non-labor cost savings by merging technology stacks, IT systems, and cloud providers, while committing to at least 30 theatrical releases per year. By 2030, the unified conglomerate targets $10 billion in free cash flow.

However, the ripple effects of this mega-merger face a formidable antitrust gauntlet. The regulatory landscape involves intense scrutiny from multiple agencies:

Department of Justice (DOJ): While the Hart-Scott-Rodino waiting period expired in February 2026, the DOJ maintains the authority to challenge the deal, specifically investigating upward pressure on pay-TV prices, the concentration of sports rights (NFL, Olympics, UFC, PGA, NCAA), and increased bargaining leverage against media workers.

State Attorneys General: California AG Rob Bonta has explicitly warned that the merger is "not a done deal," organizing a coalition to scrutinize potential job losses and consumer unaffordability resulting from the consolidation.

International Regulators: The UK's Competition and Markets Authority (CMA) and the European Commission are investigating the merger for streaming concentration and potential behavioral remedies regarding content licensing.

CFIUS: The Committee on Foreign Investment in the United States faces pressure to conduct a national security review due to the involvement of Middle Eastern sovereign wealth funds—specifically from Saudi Arabia (PIF), Qatar (QIA), and the UAE—in Paramount's financing.

Should regulatory delays push the closing past the target date of September 30, 2026, WBD shareholders are entitled to a "ticking fee" of $0.25 per share (approximately $650 million) each quarter.

Disney's Acquisition of Fubo and the Demise of Venu Sports

The live sports broadcasting sector experienced an equally dramatic realignment. In early 2024, Disney, Fox, and WBD attempted to launch "Venu Sports," a joint venture designed to bundle premium sports networks (ESPN, FS1, TNT) into a single $42.99/month streaming application. The venture posed an existential threat to independent sports-first streaming platforms like FuboTV, which subsequently launched a massive antitrust lawsuit resulting in a federal injunction that successfully blocked Venu's debut in August 2024.

Rather than endure a protracted, highly public legal battle over antitrust violations, Disney executed a calculated strategic pivot: if it could not defeat Fubo in court, it would acquire the platform and neutralize the opposition. In October 2025, Disney completed the acquisition of a 70% majority stake in Fubo, seamlessly merging it with its Hulu + Live TV business.

The settlement terms dictated that Disney, Fox, and WBD make an aggregate cash payment of $220 million to Fubo, with Disney providing an additional $145 million term loan. As part of the acquisition, the Venu Sports joint venture was permanently dissolved. The newly combined Fubo/Hulu vMVPD entity, led by Fubo CEO David Gandler, commands nearly 6.2 million North American subscribers, creating the sixth-largest pay-TV operator in the United States and consolidating Disney's absolute dominance over digital sports distribution. Coinciding with this corporate restructuring, Fubo also agreed to pay $3.4 million to resolve a separate class-action lawsuit regarding violations of the Video Privacy Protection Act (VPPA), settling claims that it shared users' private viewing data with third parties like Facebook without consent.

The Subscription Fatigue Epidemic

The relentless pursuit of streaming profitability has triggered a severe consumer backlash. The golden era of "Peak TV"—characterized by near-infinite content libraries funded by artificially low subscription prices—has ended. In its place, the industry has delivered a fragmented, highly expensive ecosystem that has resulted in acute, widespread "subscription fatigue."

Price Inflation and the Mechanics of Churn

By 2025, the average American household was spending $46 per month across an average of 2.9 streaming platforms. However, the cost of maintaining this digital footprint is accelerating significantly faster than general economic inflation or wage growth. Subscription prices surged by an astonishing 25% in the past year alone, with platforms enacting average annual rate hikes of 9%.

The calendar year 2025 and early 2026 saw a cascade of price hikes across almost every major platform:

Netflix: Implemented a widely debated price hike in January 2026, pushing its Standard tier to $19.99/month (up from $17.99) and its Premium tier to $26.99/month (up from $24.99). Furthermore, the cost to add an "extra member" outside the household increased to $7.99 (with ads) and $9.99 (without ads), meaning a Premium package with two out-of-household users can now cost a staggering $46.97 per month.

Amazon Prime Video: Increased the fee required to remove advertisements from $3 to $5 per month in April 2026.

Others: Spotify, Paramount+, Sling TV, Crunchyroll, and Amazon Music all implemented simultaneous rate hikes in the first quarter of 2026, following similar increases by Apple TV+, Peacock, and Philo in late 2025.

The consumer response to these unrelenting pricing pressures has been swift and highly quantifiable. According to comprehensive market surveys conducted by YouGov, nearly half of all U.S. adults (49%) altered their streaming subscriptions in the past six months. Among those who canceled a service, a staggering 66% cited cost as the primary factor, heavily outweighing those who canceled simply because they finished watching desired content (26%) or due to a lack of original programming (8%). When evaluating new services, 74% of consumers now consider cost the primary determining factor, compared to just 51% who focus on content variety.

Consequently, industry-wide average monthly churn rates surged to 5.5% in early 2025, a dramatic escalation from the 2% baseline observed in 2019. The market has birthed a new demographic of "serial churners"—users who subscribe to a service, binge a specific premiere, and immediately cancel before the next billing cycle. This group now represents 23% of the U.S. streaming audience. There is also a distinct generational divide in platform management: consumers aged 25–34 access an average of six platforms (often utilizing account sharing), whereas users over 55 subscribe to only three.

The "Enshittification" of the User Experience

Beyond simple price hikes, subscription fatigue is deeply compounded by a widespread degradation in perceived value. The strategic rollout of advertising into previously ad-free ecosystems, stringent crackdowns on password sharing, and the outright removal of deep library content for corporate tax write-offs have collectively eroded consumer goodwill.

Subscribers who once paid $125 a month for traditional cable fled to early streaming platforms specifically to escape advertisements and scheduled viewing constraints. Today, a comparable suite of premium, ad-free streaming applications easily approaches $70 to $80 a month, and the lower-tier options are heavily saturated with commercials. This systemic degradation of service—often referred to colloquially in tech analysis as "enshittification"—is fundamentally altering the psychological contract between streamer and subscriber. Platforms are increasingly viewed as adversarial utilities rather than beloved entertainment brands.

The AVOD Ascendancy and the Dual-Tier Economy

Because direct subscription markets have reached their absolute saturation point, media conglomerates have universally concluded that advertising is the primary incremental revenue driver for the foreseeable future. Ad-supported Video on Demand (AVOD) is no longer a supplementary feature or a concession to low-income demographics; it is the core growth engine of the global streaming ecosystem.

The Velocity of the Advertising Pivot

The speed of the AVOD transition has been entirely unprecedented in modern media history. As recently as 2019, ad-supported streaming was viewed as a secondary market, with executives at platforms like Netflix famously insisting they would never run ads. By late 2025, AVOD had become the dominant acquisition channel across the industry.

More than 70% of all net new streaming subscriptions in the U.S. since 2023 have originated from ad-based plans, equating to 27.4 million net additions in 2024 alone. On Netflix, 45% of total U.S. household viewing hours now occur on its ad-supported tier, up from 34% the prior year. Amazon Prime Video executed the most aggressive transition, moving its massive global user base onto an AVOD model by default, requiring an active opt-in and additional monthly fee to remove advertisements.

The economic rationale driving this pivot is highly compelling. While the raw ARPU for an SVOD user is nominally higher than an AVOD user, the profit margins and scalability of advertising revenue are vastly superior in a saturated subscriber market. Furthermore, ad-supported tiers create a strategic pricing "floor" that enables further monetization of premium users.

By maintaining a relatively low entry price point for ad tiers (e.g., Netflix's $8.99 plan), platforms can aggressively raise prices on their premium, ad-free tiers ($26.99) with relative impunity. Price-sensitive users facing a $20+ monthly bill are far more likely to "downgrade" to an ad-supported tier rather than churn off the platform entirely. As media analyst Robert Fishman noted, this dynamic effectively converts a lost subscriber into a highly lucrative advertising impression, reducing net churn for the overall platform while scaling a secondary revenue stream.

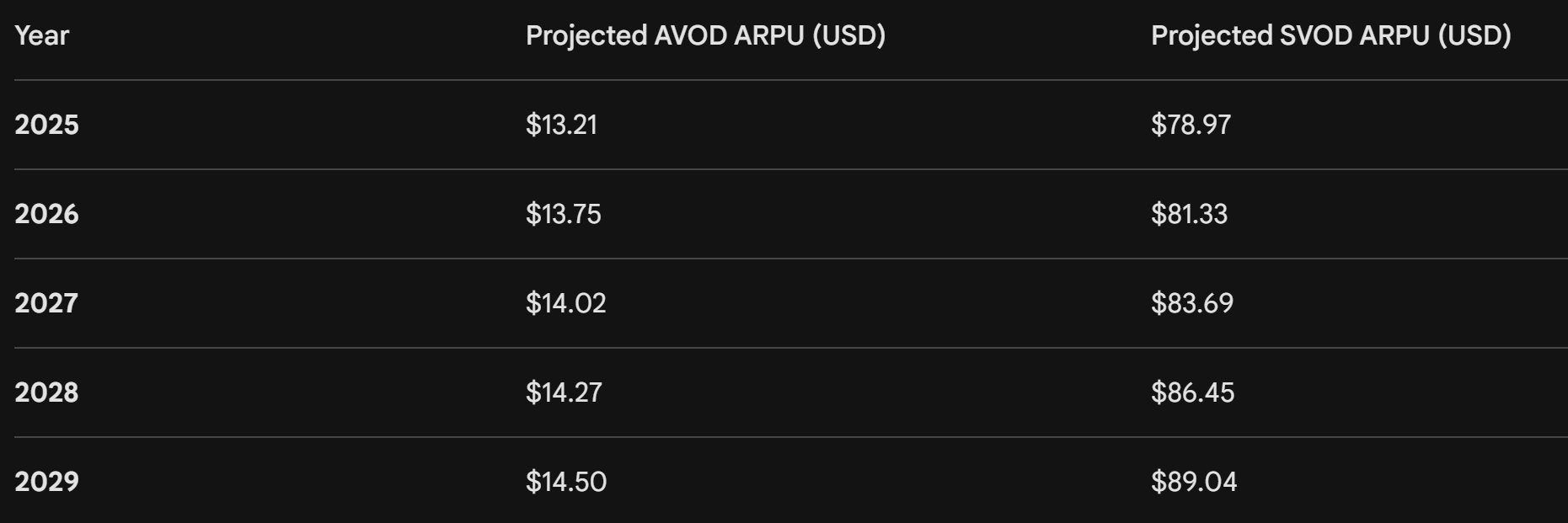

Market Value Projections: AVOD vs SVOD

Projections indicate that the aggregate revenue gap between premium AVOD and SVOD is narrowing rapidly, reshaping the allocation of global marketing budgets. By 2029, premium AVOD is projected to reach $141 billion globally, trailing SVOD at $185 billion.

ARPU reflects global averages across multiple regional pricing models.

This dual-tier economy demands entirely new corporate infrastructure. Streaming platforms must now function simultaneously as direct-to-consumer content retailers and sophisticated programmatic ad-tech vendors, bridging complex measurement gaps, integrating addressable advertising technologies, and defending against Connected TV (CTV) ad fraud.

The Great Re-Bundling: Recreating the Cable Paradigm

Faced with a 5.5% churn rate and the existential threat of subscription fatigue, the industry has realized that the most effective mechanism for retaining subscribers is the exact business model they spent the last decade violently disrupting: the cable bundle. Single-app subscriptions are inherently fragile; bundled subscriptions, tied to essential home broadband services or deeply discounted aggregator packages, create high switching costs and formidable psychological barriers to cancellation.

By 2026, 43% of all streaming platforms offered integrated bundle services, with 55% of those offerings tied directly to telecommunications or internet service provider (ISP) partnerships. The most prominent execution of this aggregation strategy is Comcast’s "Xfinity StreamSaver." Launched seamlessly through its broadband footprint, the bundle offers Netflix Standard with ads, Peacock Premium, and Apple TV+ for an everyday price of $15 a month—delivering a discount of over 30% compared to purchasing the services individually.

Similar packages have proliferated rapidly across the market:

Telecom Bundles: Verizon and T-Mobile continue to heavily subsidize streaming services to prevent mobile churn, though executives like Dan Schulman have warned that relentless price hikes by streaming partners are eroding the perceived value of these telecom bundles, contributing to Verizon losing 2.25 million net customers over three years.

Genre Packs: Platforms like AMC+ and Discovery+ bundled together for $13.99/month offer targeted demographics up to 30% savings.

Aggregator Platforms: Amazon Prime Video Channels and DirecTV stream packages allow users to manage 50+ channels and FAST integrations under a single billing architecture.

These bundles serve a critical dual purpose. For the consumer, they alleviate the mental friction of managing multiple subscriptions, passwords, and billing cycles, while offering tangible financial relief. For the streaming platforms, bundles guarantee wholesale subscriber volumes, dramatically reduce marketing and customer acquisition costs, and functionally eliminate the risk of "serial churning." A consumer is highly unlikely to cancel their entire internet-and-entertainment package simply because they finished watching a specific television series.

However, the secondary, long-term effect of the bundle is the commoditization of the underlying platforms; as services are aggregated, direct brand loyalty diminishes, and the balance of power shifts inexorably back to the distributor—a full, cyclical regression to the 20th-century pay-TV dynamic.

The Ascendance of Alternative Media: FAST and vMVPDs

While premium SVOD platforms battle over churn and bundle positioning, massive structural shifts in viewership are occurring in alternative, lower-friction ecosystems. Consumers suffering from subscription fatigue are increasingly retreating to Free Ad-Supported Streaming TV (FAST) and digital linear replacements, signaling a return to lean-back, broadcast-style consumption.

The FAST Channel Explosion

The FAST market has rapidly evolved from a repository for low-tier legacy content into a critical, multi-billion-dollar pillar of the global streaming economy. In Q3 2025, the number of active FAST channels globally grew to nearly 1,850, representing a 14% growth from Q1 2026 and an astonishing 76% expansion since 2023.

Major platforms like Pluto TV (Paramount), Tubi (Fox), and The Roku Channel account for a significant and growing share of living room television time. By late 2025, 69% of U.S. households utilized at least one FAST service. The Roku Channel alone achieved an unprecedented 3% of all U.S. TV viewing time—surpassing paid, premium platforms like Paramount+ and closing in on Amazon Prime Video's 4.3%. This viewing share translates directly into massive capital; Roku reported full-year 2025 Platform revenues of $4.145 billion, dwarfing its physical device revenues, driven by 145.6 billion streaming hours. Overall, Comscore's 2025 State of Streaming report highlighted that total hours watched across major FAST services grew by 43% year-over-year.

A sophisticated analysis of FAST content catalogs completely counters the prevailing narrative that these channels rely purely on antiquated media. FAST channels currently offer proportionally more recent programming than many premium subscription services. According to Gracenote data, nearly 80% of FAST programming was produced within the past 15 years, compared to just 68.5% on SVOD platforms. This recency, combined with the zero-friction entry point, explains why the global FAST market is projected to skyrocket from $14.33 billion in 2026 to $31.29 billion by 2031.

The Virtual Pay-TV Transition

Concurrently, the digital pay-TV market—comprising virtual multichannel video programming distributors (vMVPDs)—is quietly but decisively supplanting traditional cable hardware. Services delivering linear TV over the internet, including YouTube TV, Sling TV, and the newly merged Disney/Fubo entity, are capturing the cord-cutting demographic that still desires live news and sports.

YouTube TV’s trajectory is particularly disruptive to legacy operators. Having expanded aggressively via massive investments in live sports (notably securing the NFL Sunday Ticket), YouTube TV is forecast by research firm Omdia to reach 10.4 million to 12.6 million subscribers by 2027. This milestone will see a digital vMVPD overtake legacy giants Charter Communications (11.4 million) and Comcast (10.6 million) to become the absolute largest pay-TV operator in the United States, cementing the internet's total victory over traditional coaxial cable infrastructure.

Social Video: The Unseen Competitor for the Living Room

The traditional Hollywood studio system operates under the historical assumption that their primary competitors are rival studios. However, the most severe existential threat to SVOD viewing time and advertising revenue in 2026 originates from social video platforms. The dichotomy between user-generated content (UGC) and premium studio content has entirely collapsed in the eyes of the modern consumer.

YouTube and TikTok are no longer confined to mobile devices; they have successfully and aggressively colonized the living room television screen. YouTube is currently the dominant force in U.S. television, commanding 12.5% of all TV use in May 2025—the highest share of any streamer to date. Market data from Parks Associates reveals that social video now accounts for 4.9 hours per week of TV viewing, capturing 20% of all video consumed on traditional television sets, surpassing time spent watching traditional broadcast video.

The generational metrics underlying this shift are deeply alarming for legacy media conglomerates. Among viewers aged 18–34, social video consumption nearly matches SVOD viewing on TVs and vastly exceeds SVOD on mobile devices. Over 40% of this demographic watches more than 15 hours of social video per week. Gen Z users now spend 54% more time per day on social platforms watching UGC than the average consumer, and 26% less time watching traditional TV and movies.

Furthermore, TikTok's global user base continues to mature, moving far beyond short-form lip-syncs to longer-form content. The platform's new Creator Rewards Program mandates videos over a minute in length, resulting in users logging 10+ sessions a day averaging 10 minutes each. Conversely, YouTube viewing sessions average 40 minutes, mirroring traditional episodic television consumption. YouTube Premium has also seen massive growth, jumping from 100 million users in 2024 to 125 million in 2025, indicating that consumers are increasingly willing to pay directly for creator-led content over studio-produced series.

Because social platforms are algorithmically optimized for hyper-engagement and carry minimal content production costs compared to Hollywood studios, their profit margins are vastly superior. As premium streamers struggle with massive debt loads from prestige television production, social video platforms are capturing the majority of global digital advertising spend, fundamentally disrupting the economic models that studios have relied upon for decades.

The Resurgence of the Jolly Roger: Digital Piracy in 2026

The early, utopian promise of the streaming revolution was that supreme convenience and affordability would organically eradicate digital piracy. For a time, this hypothesis held true; piracy metrics reached historic lows around 2020 as platforms like Netflix offered vast, centralized libraries for a nominal fee. However, the intense fragmentation of content across dozens of siloed apps, coupled with runaway price inflation, the insertion of advertising into paid tiers, and the "enshittification" of the user interface, has systematically driven consumers back to the black market.

The Economic Scale of Modern Content Theft

By 2025, global visits to digital piracy websites surged to an estimated 216.3 billion, a dramatic and sustained increase from 130 billion just five years prior. The composition of this illicit traffic reveals a massive appetite across all media formats: TV piracy accounted for 96.8 billion visits, publishing 66.4 billion, film 24.3 billion, and music 13.9 billion. Unlicensed streaming portals—as opposed to traditional, easily trackable file-sharing torrents—now account for a staggering 96% of all TV and film piracy, presenting viewers with interfaces that often rival the UX of legitimate platforms.

The macroeconomic devastation is profound. The global media and entertainment industry loses an estimated $75 billion annually to digital theft, a figure projected to scale to $125 billion by 2028 as content remains heavily fragmented. The United States video industry alone suffers between $29.2 billion and $71 billion in annual losses. In tech-forward regions like Sweden, 25% of the population openly admits to pirating content, heavily indexed among the Gen Z and Millennial demographics, where up to 76% admit to utilizing illicit sources. Furthermore, digital piracy is now a major data load contributor, accounting for 24% of bandwidth use in key regions.

As Gabe Newell famously stated, piracy is rarely a pricing issue; it is a "service issue". The 2026 consumer views piracy not as a malicious criminal act, but as a highly rational economic response to artificial scarcity. When viewers are forced to subscribe to three different platforms to follow a single cinematic universe, or when regional geoblocks require the use of VPNs just to access basic content, the frictionless nature of illicit streaming sites becomes deeply appealing.

This behavioral economics principle is violently exacerbated by franchise releases. Exclusive data from MUSO highlights that new theatrical releases in massive franchises (such as Jurassic World or Mission: Impossible) trigger massive, immediate spikes in the piracy of back-catalog titles extending back to the 1990s. Viewers actively refuse to pay multiple SVOD tolls to catch up on preceding narratives just to understand a new theatrical release, immediately defaulting to piracy for older titles.

The Evolution of Infrastructure Parasites

Combating this resurgence is severely complicated by the technological sophistication of modern pirate networks. The industry is currently battling a highly advanced phenomenon known as "infrastructure parasites" or Content Delivery Network (CDN) leeching.

Rather than building their own expensive server farms and absorbing the costs of bandwidth, advanced pirate syndicates exploit vulnerabilities in the legitimate streaming infrastructure of major platforms. They functionally hijack the CDNs of actual streaming providers to deliver stolen content to their illicit subscriber bases at virtually zero distribution cost. This bypasses content creation and licensing costs while exploiting the providers' own servers, making detection incredibly difficult.

In response, studios and networks are forced into a costly technological arms race. The global anti-piracy protection market was valued at $236.2 billion in 2025 (reflecting a 12.3% YoY growth) and is forecast to reach $754.9 billion by 2035. Industry surveys reveal that nearly 80% of security professionals view Digital Rights Management (DRM) and dynamic watermarking as the absolute preventive backbone of content security, while 43.6% identify AI-driven internet pattern monitoring as the highest-impact solution for identifying pirate hotspots in real-time.

The AI Mirage: The Collapse of Sora and Hollywood's Cost Realities

A pervasive, highly influential narrative throughout 2024 and 2025 was that generative Artificial Intelligence (AI) would drastically lower the exorbitant production costs that were financially crippling the streaming industry. The focal point of this extreme techno-optimism was OpenAI’s video-generation model, Sora, which sparked both intense labor fears and corporate excitement across Hollywood that everything from complex background generation to entire animated sequences could be outsourced to algorithms.

This belief was institutionalized when The Walt Disney Company announced a highly publicized, billion-dollar equity and licensing agreement with OpenAI, designed to integrate Sora directly into Disney's creative pipeline to generate fan-inspired short videos and reduce reliance on traditional rendering pipelines.

However, the reality of deploying generative video at a commercial scale failed to align with the rampant technological hype. In early 2026, OpenAI abruptly and unceremoniously shut down the Sora program prior to a wide global launch. The internal logic for the shutdown was multi-faceted: the compute costs to generate high-fidelity video were astronomical, the consumer-grade monetization model proved non-viable compared to API licensing, and the company chose to execute a ruthless strategic pivot toward enterprise AI products, coding tools, and agentic systems.

The immediate corporate consequence was the total collapse of the $1 billion Disney-OpenAI partnership, which had not fully closed before the technology it relied upon was shelved. This failure represents a critical, sobering reckoning for the streaming industry's financial models. Streaming executives had quietly factored long-term, AI-driven cost reductions into their five-year paths to profitability. With the immediate promise of frictionless, high-fidelity AI video generation evaporating, studios must accept that the hard costs of premium content production—labor unions, physical production logistics, and intense VFX rendering—will remain stubbornly high. Consequently, the pressure to extract value directly from the consumer via continuous subscription price hikes and ad-density increases will only intensify, further fueling the cycle of subscription fatigue.

Concluding Analysis: The New Rules of the Streaming Economy

The media landscape of 2026 reveals an industry that has survived its own highly destructive era of disruptive innovation, but remains permanently scarred by the economic fallout. The halcyon era of the "Streaming Wars" was defined by aggressive global expansion, unprecedented content gluttony, and the arrogant belief that direct-to-consumer software could entirely bypass traditional distribution bottlenecks and consumer pricing sensitivities. The harsh reality of 2026 proves the exact opposite: the fundamental, gravity-like laws of media economics remain unbroken.

Several undeniable truths now govern the entertainment sector:

Scale is the Ultimate Moat: The Paramount/WBD merger and Disney's aggressive consolidation of Fubo demonstrate that mid-tier platforms cannot survive stand-alone SVOD economics. Consolidation will continue unabated until only three to four truly global mega-platforms remain, operating as sprawling digital utility companies rather than boutique studios.

The Bundle Always Wins: The fragmentation of media caused far too much friction for the average consumer. The rapid return to telecom-backed bundles and ISP aggregation proves that the traditional "cable model" is highly efficient for churn reduction, lifetime value optimization, and consumer psychological comfort.

Advertising is the Bedrock: The dream of premium, ad-free television at scale is definitively dead. AVOD and FAST channels are the dominant forces of viewership and revenue growth, pushing pure SVOD back into a luxury, niche commodity for high-income demographics.

Attention is the True Currency: The historical line dividing Hollywood and Silicon Valley has blurred into nonexistence. Streaming platforms are no longer just fighting each other for subscription dollars; they are engaged in a vicious, zero-sum war for raw screen time against the algorithmic dominance of YouTube, TikTok, and the frictionless appeal of illicit pirate networks.

Ultimately, the streaming industry has successfully transitioned audiences away from traditional linear broadcasting, but in doing so, it has systematically recreated the linear TV business model on the internet—complete with unskippable commercials, highly restrictive bundled packages, and frequent, punishing price hikes. For the consumer, the streaming revolution has simply brought them back to exactly where they started, albeit at a significantly higher premium and distributed across a far more complex technological landscape.